The State of Curve.

The “crab” price action continues. The current rebound in $BTC and altcoins doesn’t seem sustainable. Therefore, there isn’t much to add about the state of the market. Instead, let me share the overview of potential risks for Curve by Sergey.

The following text doesn’t suggest that Curve is a bad project but highlights potential predicaments that every holder will benefit from knowing. Here it goes.

It is hard to imagine the future with Curve failing or disappearing completely from the DeFi landscape. Since its launch, the project has become essential for other protocols for creating trading venues for their native assets.

As you may already know, Curve pools are incentivized with $CRV emissions that token holders direct to different pools. The more trading volume the platform generates, the higher income goes towards $CRV stakers. Hence, there is a direct correlation between trading volume/platform usage and $CRV demand. Curve is one of the few protocols where holders receive income that doesn’t come from pure token inflation.

The Crypto industry is a highly innovative and competitive environment. Looking retrospectively at projects by market caps, projects that were in the top 50 are now replaced by more relevant competitors.

If we look at current DEX niche players, the closest competitor to Curve is Uniswap. Its recent v3 upgrade allows liquidity providers to earn fees more efficiently by providing liquidity in narrow price ranges, which is very similar to Curve’s model.

The volume on Uniswap consistently surpasses Curve, which suggests that Curve is losing its business to it. However, $UNI is useless besides pure protocol governance.

In contrast, $CRV gives access to cash flows. That’s why DAOs and other stakeholders still require $CRV to ensure high liquidity for their native pegged assets even in the current environment.

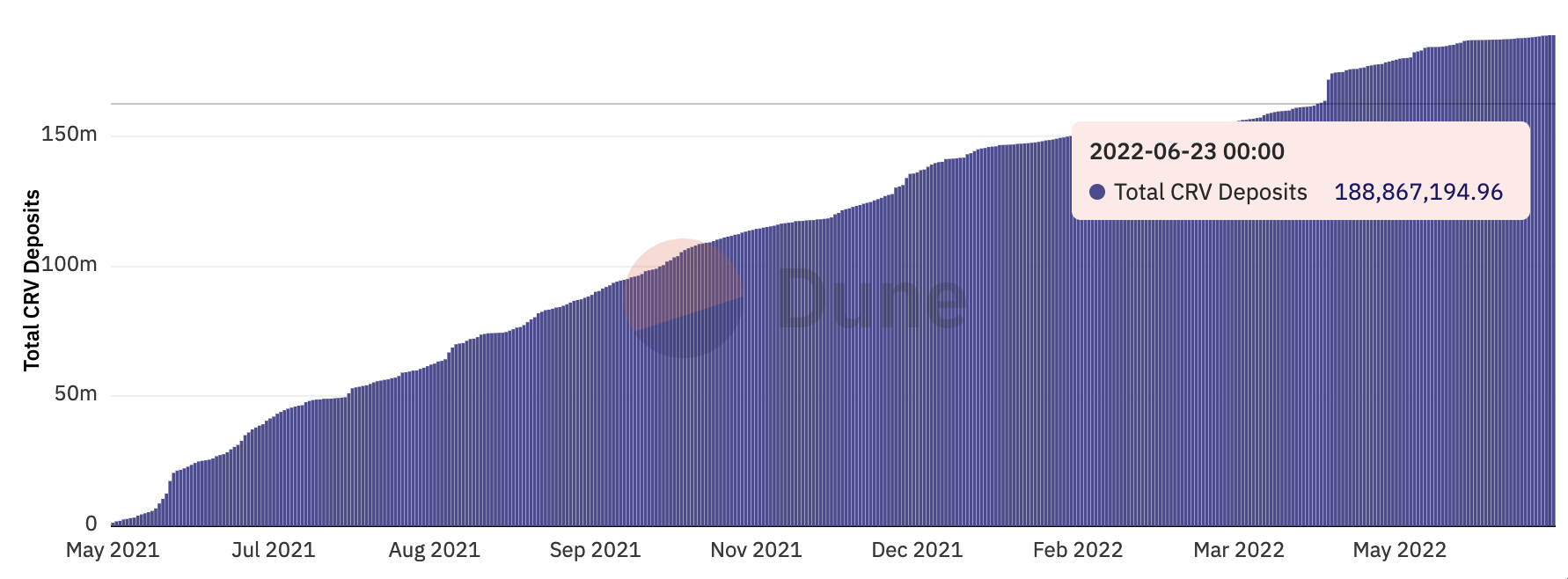

Convex alone attracts millions of $CRV. Source: Dune.

Given that Uniswap Labs is a US-based company, it’s unlikely to revise its current tokenomics in favor of token holders. That’s because income coming directly to holders may deem $UNI security. Therefore, Curve remains a more lucrative investment than Uniswap despite processing less trading activity.

Still, other exchanges are implementing Curve’s tokenomics. Balancer has recently moved to the voting escrow in the attempt to create a Curve-like flywheel within its ecosystem. However, given Balancer’s flexibility and a broader focus product-wise, Curve can surely coexist with it without losing its business.

There have been other attempts to create an “improved version” of Curve. The relatively recent attempt by Andre Cronje called Solidly failed mainly due to contract flaws and malicious parties involved in governance upon launch. Velodrome tried to revive Solidly ideas on Optimism, but due to current market conditions, the protocol can’t attract sufficient capital and generate high volumes to present a threat.

As mentioned above, the industry is highly competitive, and the “Curve” killer may indeed appear one day. However, with Curve’s current large ecosystem and “Curve Wars” flywheel, it would seem nearly impossible to take its spot. After all, that is what ve tokenomics is designed to do: keep capital sticky with the platform.

As mentioned above, $CRV holders receive the income generated from trading volume. If volumes drop considerably over time, which might happen due to poor market conditions, the demand for $CRV will decline too.

Currently, it still makes sense to use Curve and Convex for liquidity management for other projects. That’s because $1 spent on bribes results in $1.25 worth of emissions. Thus, it’s a better choice than going the old route of printing excessive amounts of native tokens.

Source: Llama Airforce.

If this metric stays below $1 for too long, some projects may be tempted to pivot from Curve, which can create substantial pressure on $CRV and cause other projects to get rid of their holdings.

However, a significant portion of $CRV is locked for years, which should help alleviate some selling pressure. Moreover, $CVX staked ratio is still above 80% even in the current market conditions.

The reason? Liquidity management has to change. It has to go from the hands of individuals to protocols. Projects like Curve, Redacted Cartel and Tokemak arrange their business models around that. That’s why other projects will likely stick with these tokens and even accumulate them at lower prices to have the upper hand in terms of liquidity management once the bullish sentiment returns.

SIMETRI Portfolio – A Rebound Wasn’t Enough

A cascade of liquidations that occurred last weekend pulled down the portfolio. Even though the altcoin market cap rebounded since then, it wasn’t enough to bring the portfolio the previous ROI.

Disclosure: The author of this newsletter holds ETH. Crypto Briefing and members of the research team hold some of the Pick of the Month coins mentioned in the table above. Read our trading policy to see how SIMETRI protects its members against insider trading.